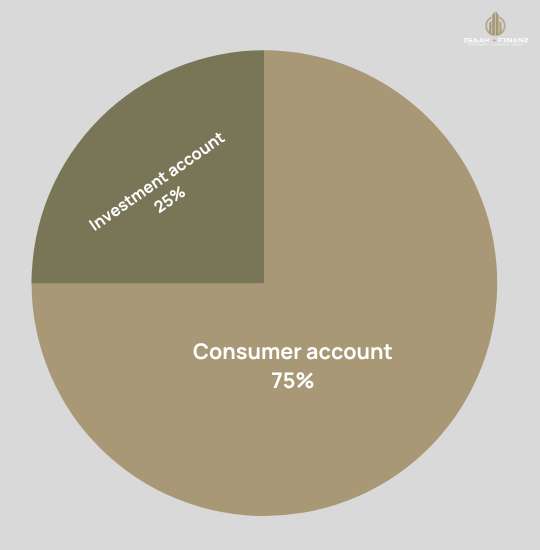

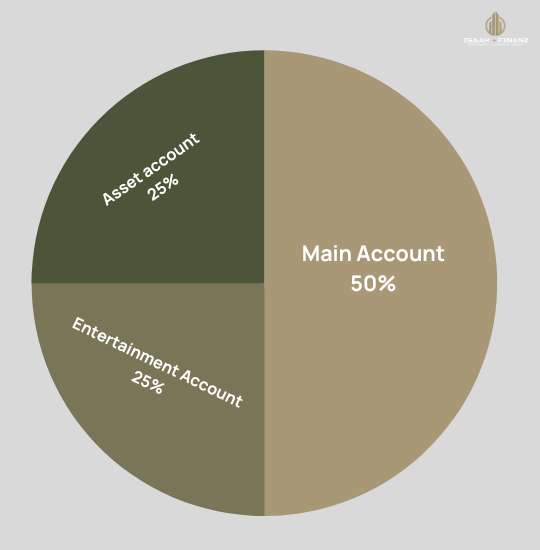

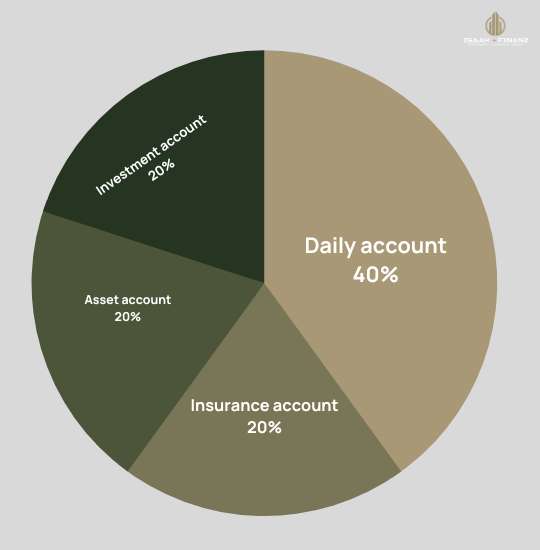

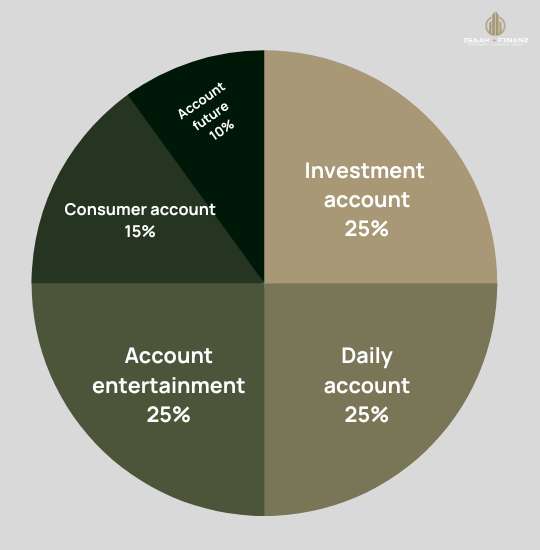

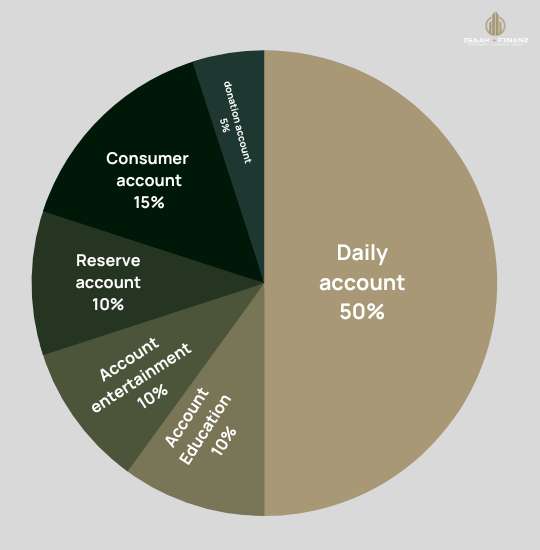

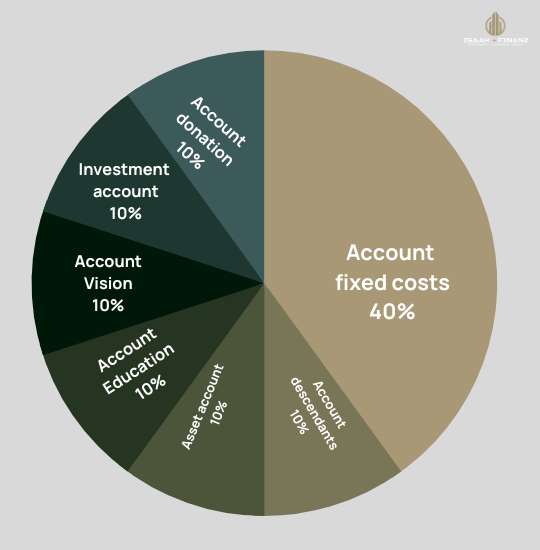

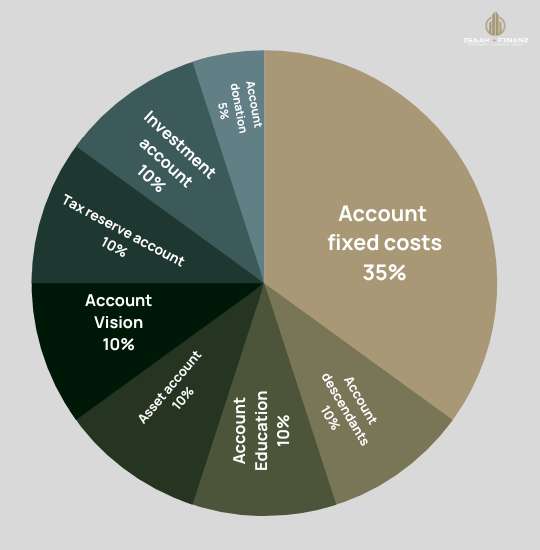

It is a financial model of a multi-account strategy for different areas in which you allocate your income.

There are many different account models that financial analysts have developed.

Not all models are suitable for everyone. You should choose the one that is most accessible to your situation.

Don't let all of this scare you... that's where I take over with transparency and no hidden costs to help you choose the model that fits you and gets you closer to financial freedom!